In 1933, the United States devalued its currency by 75% (against gold) in order to combat the relentless deflation of the Great Depression. China will eventually use the same strategy to get out of its own depression.

In the 1920s, the British wanted to return to the pre-war gold standard. Having run up a huge debt to finance the war though, the pound should have devalued versus gold; instead the pound was intentionally overvalued. The U.S., the world's largest exporter at the time, cooperated with Great Britain and inflated its currency to aid Great Britain's economy.

In the late 1990s and into the 2000s, China, one of the world's largest exporters, inflated its currency (through the currency peg) and aided the U.S. economy. China was to the U.S. as the U.S. was to Britain in the 1920s.

In the 1920s, European countries could not easily export to the U.S. due to tariffs (and the undervalued U.S. dollar). Instead they financed their imports with loans from America. In the 2000s, Americans could not export to China due to, among several factors, tariffs and an undervalued yuan. Instead they financed their imports through loans from China (via the Treasury market).

In both cases, there were huge buildups of reserves: gold flowed to the United States, U.S. dollars flowed in China. Both nations had huge overcapacity because they were providing a huge portion of global production. When the U.S. went into a depression and nations began devaluing their currencies, they quickly exited the depression because the could no longer afford U.S. imports and began producing for themselves. Today, China is loaded with overcapacity aimed at global markets that may very well close to them in a global recession or depression.

Chinese Inflation

Back when the Chinese yuan was pegged at 8.28 to a U.S. dollar, whenever a U.S. dollar entered the Chinese financial system, it was exchanged by the People's Bank of China (PBOC) for 8.28 renminbi. Most economists and analysts believed the yuan was undervalued at the time, but there was a lot of disagreement about how much it was undervalued. At best, I can say that had the peg had been maintained, eventually the real value of the Chinese yuan would reach that exchange rate of 8.28 to $1 and even move lower thanks to galloping inflation.

So was the yuan over or undervalued before it began rising in 2005? Almost everyone said it was undervalued, but what was the real value? At the time there were many numbers bandied about, many were in the range of 20-40% undervalued. Say it was 30% in 2005, just as the yuan was allowed to float. That means the real value of the yuan in 2005 was about 5.8 to 1, when the yuan began to rise from 8.28 to $1. At 6.1 yuan to 1 dollar the currency is still weaker (versus the U.S. dollar) than it was in real terms in 2005, and yet the Chinese central bank and government have stated in the past year that the yuan is "fairly valued." (03/12/2012 China's yuan nearing fair value: PBOC's Zhou ) Therefore, in real terms, depending on your initial value for the yuan, it may actually have fallen in real value since 2005 or been flat relative to the U.S. dollar.

So has the yuan been appreciating or depreciating in real terms? The central bank still maintains a dirty peg: it allows the yuan to trade in a band around a price set by the central bank. While the market is increasingly allowed to set the value within the band, it is only allowed to do so within the confines of the central bank policy and China clearly had political reasons to allow the renminbi to rise versus the U.S. dollar. By 2008 there was a growing risk of trade retaliation by the United States, in 2012 it was a topic of the Presidential campaign and in 2013 the EU is implementing anti-dumping tariffs on Chinese solar panels, with calls for more tariffs on Chinese goods. Since China's leaders can more easily exchange between political and economic costs, we should be open to the possibility that the yuan has a far larger political component to its value than other currencies.

The Yuan Has Depreciated Before

In 2008, China ceased appreciation of the renminbi and went back to a fixed U.S. dollar peg. Not to defend the economy from the currency's rise, rather to protect it from falling at a politically insensitive time and preventing its collapse along with other emerging market currencies that had been leveraged against the U.S. dollar. China did the same thing in 1997, refusing to devalue during the Asian Crisis.

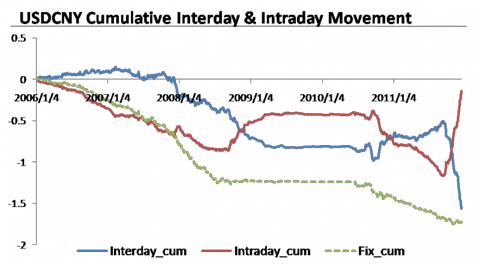

But consider this chart (Source: Interday and Intraday Movement of USDCNY). From the link: In this chart, the green dashed line stands for the cumulative movement of USDCNY central parity, or fixing price, since 2006. The red line shows the cumulative result of USDCNY intraday movement, i.e. the difference between today's close and fixing. In contrary, the blue line is the cumulative result of interday movement, or the difference between fixing and last day's close price.

(click to enlarge)

What the chart shows is that there were periods in 2008/2009 and again in 2011 when traders were pushing the yuan down on a sustained basis, but the central bank was pulling yuan higher by adjusting the exchange rate (the fixing or the midpoint in the trading band).

This is clear evidence that the Chinese yuan is either fairly valued or at least experiences selling pressure from time to time. In light of this, consider the latest rally in the yuan which has been artificially driven by currency arbitrage (How Fake Exports Caused The Yuan Rally). Exporters are feeling the pinch, particularly as China's trading partners see their currencies devalue against the U.S. dollar. Investors often focus on the USDCNY exchange rate, but the movement in the dollar versus other currencies is still more important for China than the movement of the yuan versus the dollar. The yuan's rally is coming on top of gains in the U.S. dollar versus many emerging market currencies.

Now, add in debt. Recently, I came across this article by Charles Dumas, Chairman of Lombard Street Research: Markets Insight: Weaker yen could burst China's asset bubbles. The conclusion is that the yuan may be overvalued by 33%, which implies an exchange rate of 8.11 yuan to 1 dollar. This isn't surprising if you believe the Chinese economy has relied on an expansionary monetary policy and is surprisingly close to the 8.28 peg from last decade. f emerging market currencies continue to depreciate versus the U.S. dollar (and thus the Chinese yuan), the amount of devaluation needed will increase.

Credit Growth

The parallel with the 1920s U.S. economy is clear: an exporter to the world with an undervalued currency. In the 1920s, England refused to accept that WWI costs left the pound in need of devaluation and re-pegged it at the old rate, leaving the U.S. dollar undervalued. The result was a boom in American exports, credit growth and U.S. gold reserves. In the 2000s, China undervalued its currency relative to the U.S. dollar, resulting in a boom in Chinese exports, credit growth and Chinese forex reserves. The fallout from this policy was a major economic depression in the United States and an eventual 75% devaluation of the U.S. dollar in 1933.

Instead of facing the music in 2008, China doubled down and unleashed a monster credit boom in 2009. This extended the boom for several more years, but it will not continue forever, and some analysts are already forecasting China's Minsky Moment, when cash flow is insufficient to service debt and rising asset prices are required. (Is This China's 'Minsky Moment'?)

What about the reserves?

China's currency reserves are considered a sign of strength, when in fact it was the result of a an undervalued yuan. If the Fed declared tomorrow that it would pay $5,000 cash for every oz of gold, the Fed would corner the gold market and reserves would grow. Those gold reserves would not be a testament to sound economic policy though, they would shine as a golden reminder of a massive inflation in money supply. Chinese reserves are a testament to the inflation created in the economy, inflation that fueled a massive housing bubble and infrastructure boom that has created all manner of debt financing. If and when there is a crisis, China may need to spend those reserves to defend the value of the currency.

China hasn't yet been forced to defend the value of the yuan because it hasn't allowed a full two-way flow in capital. The massive reserves stand ready to protect the value of the currency if need be, but they also serve as a piggy bank for the government to bailout the banking system. And some of those reserves are being invested in a pro-cyclical manner. Whatever you may think of China's long-term prospects, their investments in commodity-linked companies and countries is a bet on Chinese economic growth. If China suffered a major recession or depression, those investments would collapse in value and the government would either sell at a massive loss, or be forced to sell U.S. Treasuries should there be an outflow of capital.

Most people think China's central bank selling U.S. dollars is bullish for the yuan, but this is only true when they are selling from a position of strength. When China swaps dollars for euros, yen, gold or oil, it is positive for the yuan/dollar exchange rate. However, the further they diversify away from the dollar, the greater the potential volatility in the yuan/dollar exchange rate. The U.S. dollar remains the world's reserve currency and the world is very short of dollars (a dollar debt is a dollar short position).

When dollars flow out of China, it may be due to private demand. If a depositor wishes to buy dollars, they can go to any bank and get them. In the 1997 Asian Crisis, Thailand was selling U.S. dollars like mad and it was not good for the Thai baht. If Chinese and/or foreigners demand U.S. dollars more than yuan, the result will be a flow of U.S. dollars out of China that will sink the yuan.

How Stable Are Reserves?

China's large forex reserves have two historic comparisons: the U.S. in 1929 and Japan in 1989. (Never short a country with $2 trillion in reserves?) Monetary policy in 1920s America and Great Britain parallels that of China and America in the 2000s. While some China bulls dismiss the bearish talk on China's debt situation, the Chinese are not so sanguine. In an Instablog post, Could China's $3.2 Trillion Forex Reserves Be Gone In 5 Years?, I wrote:

Tan Yaling, head of the China Research Institute of Foreign Exchange says there was a recent article stating that if the only way China can stimulate the economy is through investment, then China's $3 trillion in foreign exchange reserves will be exhausted within 5 years.

She says speculation is the greatest threat to China's development and this speculation could exhaust China's reserves. Although China has $3.2 trillion in reserves, it isn't enough to protect it from hot money, not when the global forex market trades $5-6 trillion each day. If there is no long-term strategy to defend the reserves, they could be rapidly exhausted.

We've seen the price of infrastructure investment in China's rising debt levels, and we saw those speculative flows in April. Speculators sent the yuan higher, but they can just as easily send the yuan tumbling because the arbitrageurs don't care about the direction of the currency. Two things to keep in mind: the global economy wasn't in the midst of a major recession or financial crisis in April, and the Chinese government is committed to making it easier to exchange its currency. Even more volatile moves will be possible in the future.

Finally, if China decides it will pursue quantitative easing and flood the system with liquidity, it will have to create new money, a defacto devaluation of the yuan against its reserves. If the market responds to this change by demanding U.S. dollars, the defacto devaluation of the yuan will accelerate. China would have two choices: allow the yuan to depreciate and end the outflow of forex reserves, or try to hold the peg and hope that the storm passes before reserves suffer a critical loss and a currency collapse.

Investment Implications

Is the yuan going to fall 50%? When thinking about the non-linear effects of the financial markets, it isn't impossible. Much of the global economy and financial markets are all positioned for a rising yuan. Psychologically, the world is expecting a rising yuan. The odds of a crisis remain low, but if one begins, it will be large because most investors are on the other side of the trade. If China experiences a crisis, it will not be contained, but be far more volatile precisely because the economy and currency have been sheltered from market forces. Even without a major crisis, the pressure on the yuan will push it towards devaluation against the U.S. dollar in the future, not appreciation. That said, if analysts already think the yuan could be 30% overvalued, a decline to 50% would not be out of the cards.

If the Chinese economy experienced a major recession and currency devaluation, the U.S. dollar would be the main beneficiary globally, as devaluations spread across most emerging markets. This could be happening now with Brazil, India and Australia among the nations experiencing currency depreciation versus the U.S. dollar (and Chinese yuan). China's financial system is also showing signs of a crackup, with overnight interest rates hitting 13%.

Investors can use 2008 as a template. The U.S. dollar will rally strongly against most currencies. Commodity prices will continue to weaken.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/base/copper-d.gif)